Insurance can be a difficult landscape for small business owners to navigate, especially when you’re focused on building a business rather than decoding policy language. However, there are a few essential insurance basics that all business owners need to understand, with general liability insurance being one of the most important.

General liability insurance offers baseline protection against a range of everyday risks that businesses regularly face. In this guide, we’ll go over everything you need to know about general liability insurance for a small business, including what it covers, what it doesn’t, and how to decide if your business needs it.

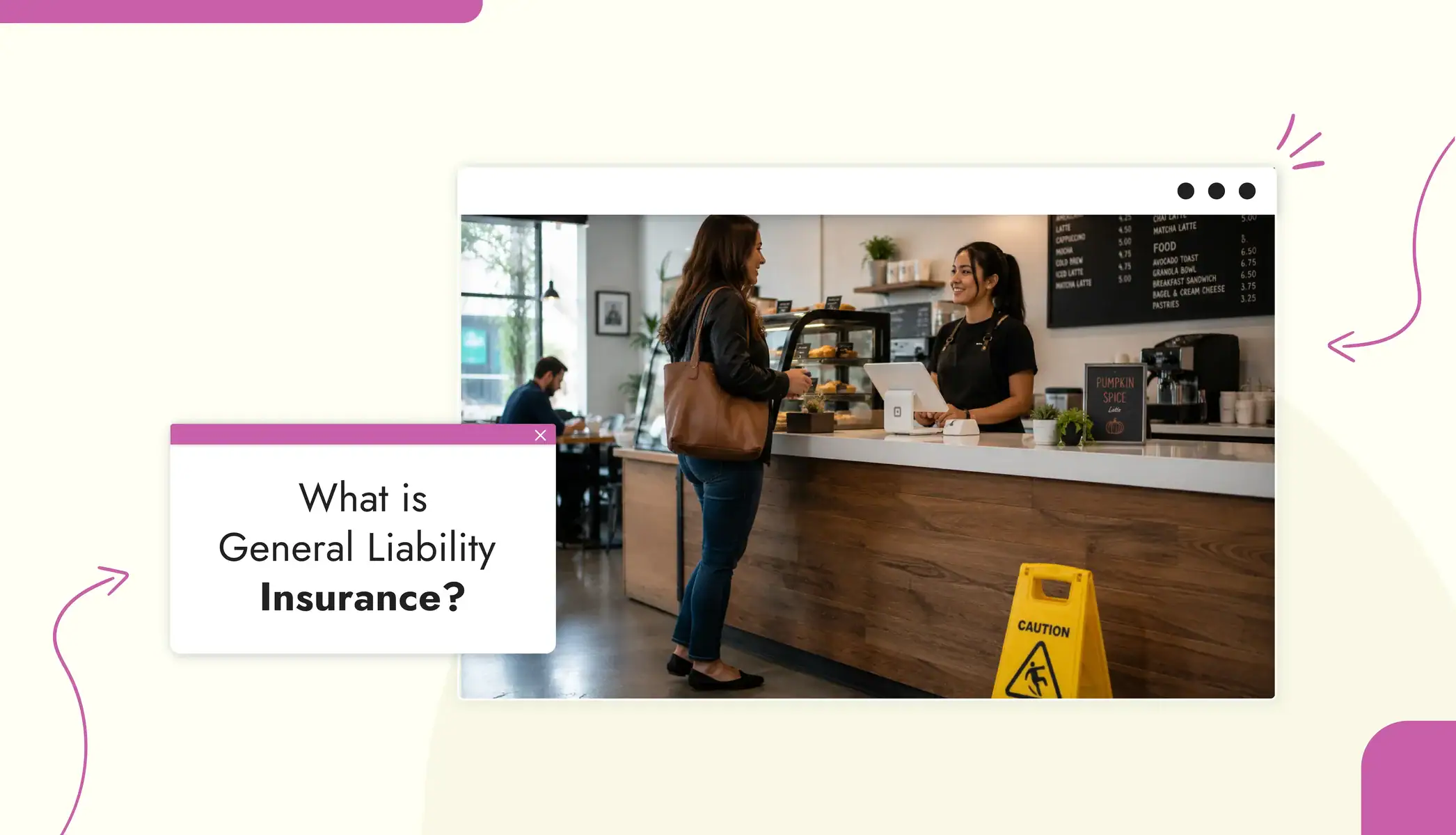

What is general liability insurance?

General liability insurance is one of many types of business insurance that helps protect your company from financial losses related to things like lawsuits, injuries, and property damage claims. If your business is held responsible for harming someone or damaging their property, general liability insurance can help cover legal costs, settlements, and medical expenses associated with that claim.

It’s worth being clear about what this coverage is designed to do: it protects the business from specific types of third-party claims. It does not cover every risk your business might face, and the specifics of what’s covered will always depend on the specific policy that you purchase.

What will general liability insurance cover?

General liability insurance is generally designed to cover the most common types of claims that businesses encounter. Here’s what most standard policies include:

- Bodily injury claims: If a customer or any other third party is injured in connection with your business, general liability insurance can help cover their medical expenses and any legal costs if they file a lawsuit. Slip-and-fall incidents on business property are one common example.

- Third-party property damage: If your business operations cause damage to someone else’s property, general liability coverage can help pay for repair or replacement costs and any related legal expenses.

- Personal and advertising injury: This coverage protects you against claims related to libel, slander, defamation, or certain copyright-related claims that arise from your business’s advertising or communications. If a competitor or individual claims your marketing caused them harm, this portion of your policy may apply.

- Legal defense costs: Regardless of the outcome, defending against a lawsuit can be expensive. General liability insurance typically covers attorney fees, court costs, and other legal expenses for covered claims, even if the case is ultimately decided in your favor.

- Medical payments: Many policies include coverage for medical expenses incurred by a third party due to a covered incident, sometimes regardless of whether the business is found legally at fault.

It’s important to keep in mind that every policy will have its own limits and exclusions. Coverage only applies to claims that fall within the policy’s defined scope, and only during the active policy period.

General liability insurance examples

Understanding how small business general liability insurance works in practice makes it easier to decide if it’s the right choice for your business. Here are a few real-world examples that illustrate when general liability insurance typically comes into play:

- A customer visits your retail shop, slips on a wet floor near the entrance, and breaks their wrist. They file a claim for medical expenses and lost wages.

- A contractor working at a client’s home accidentally knocks over a bookshelf and damages expensive equipment underneath it. The client seeks compensation for the damaged property.

- A small marketing agency runs an ad campaign that a competitor claims defames their company. The agency faces a lawsuit alleging reputational harm.

- A cleaning service employee damages the flooring in a client’s home while moving furniture during a routine job.

In each case, general liability insurance may help cover legal fees, settlements, or medical costs related to the claim. Just keep in mind that these are general examples; whether a specific incident is covered always depends on the terms of your actual policy.

What general liability insurance does not cover

General liability insurance is not all-purpose protection. There are several significant gaps that business owners should understand before assuming they’re fully covered.

Here are a few examples of claims that general liability insurance does not cover:

- Professional errors and negligence: If a client suffers a financial loss because of a mistake you made while performing a professional service, general liability insurance typically does not cover that claim. This type of risk falls under professional liability insurance (sometimes called errors and omissions (E&O) insurance).

- Employee injuries: If one of your employees is injured on the job, general liability insurance does not apply. Workers’ compensation insurance is the coverage designed to handle employee injury claims, and it is legally required for most businesses that have employees.

- Your own business property: General liability insurance covers damage to other people’s property, not your own. So, for example, If a fire damages your office equipment or inventory, you would need commercial property insurance to cover that loss.

- Commercial vehicle accidents: Accidents involving vehicles used for business purposes are not covered under a general liability policy. Commercial auto insurance handles those situations.

- Intentional acts: Claims arising from deliberate wrongdoing or intentional misconduct are excluded from coverage.

As a business grows, many owners find that combining multiple policies provides more complete coverage. Professional liability, workers’ compensation, commercial auto, and commercial property insurance each address risks that general liability insurance alone does not cover.

Do I need general liability insurance for an LLC?

This is one of the most common questions new business owners ask, so it’s worth addressing clearly: forming an LLC does not replace the need for business insurance.

An LLC, or limited liability company, is a legal structure that can help protect your personal assets from certain business debts and lawsuits. What that means is that if your business is sued, your personal bank accounts, home, and other assets generally have a layer of protection. However, that protection has limits and does not eliminate the business’s own risk exposure.

General liability insurance protects the business itself from the costs of covered claims, including legal defense costs that could otherwise drain your business’s accounts. Despite these risks, 90% of small business owners aren’t confident their companies are adequately insured, which can leave major coverage gaps unnoticed until a claim actually occurs.

In some situations, general liability is a requirement for LLCs. For example, clients, particularly larger companies, often require proof of coverage before entering into a contract, and contractors and event venues may also require it as a condition of doing business.

Which businesses benefit most from general liability insurance?

Any business that interacts with customers, clients, or the general public carries some exposure to liability claims. That said, certain types of businesses face more risks than others and are particularly likely to benefit from general liability insurance.

Retail stores, restaurants, and any business that receives a lot of foot traffic are more exposed to bodily injury claims. Contractors, tradespeople, and service businesses who work on client properties face both injury and property damage risk. Businesses that rent commercial space often have landlord requirements to meet. Event-based businesses that bring together large groups of people face heightened injury and property risks.

Even businesses that operate primarily online or in lower-risk environments can still face advertising injury claims or situations that lead to lawsuits. The cost of legal defense alone makes liability coverage worth considering, no matter what type of business you own.

How much does general liability insurance cost?

The cost of general liability insurance varies considerably depending on the nature of your business and the amount of coverage you need. Many small businesses with lower risk profiles pay somewhere in the range of $400 to $1,500 per year, with higher-risk businesses typically paying more.

There are several factors that influence how much you’ll have to pay:

- Industry: Businesses in physically demanding or higher-risk fields, such as a construction business or event services, typically pay more than those with lower risk profiles.

- Location: Regional differences in legal costs and claim frequency can affect premiums.

- Revenue: Larger businesses tend to face higher premiums due to the fact that they have greater exposure.

- Number of employees: More employees generally means more potential for claims.

- Claims history: A history of past claims can increase your premiums.

- Coverage limits: Higher limits and lower deductibles increase the cost of a policy.

Getting multiple quotes from different insurers is the best way to determine what coverage will cost for your specific situation.

When businesses choose a business owner’s policy (BOP) instead

Many small businesses, especially those with physical locations or significant assets, opt for a business owner’s policy (BOP) instead of purchasing general liability insurance on its own.

A BOP bundles general liability insurance, commercial property insurance, and business interruption coverage into a single package. Business interruption coverage can help replace lost income if your business has to temporarily close due to a covered event such as a fire or natural disaster.

BOPs are often more cost-effective than purchasing each type of coverage separately, and they streamline the process of managing multiple policies. Not every business needs a bundled policy, but for those that do, a BOP is worth exploring.

Preparing your business before getting liability insurance

Before applying for general liability insurance, it helps to have your business information organized and accessible. Insurance providers evaluate your business structure and operations when determining eligibility and pricing, and having clear documentation makes that process smoother.

Useful information to have on hand includes your business’s legal structure, employer identification number (EIN), a clear description of your business activities, and basic financial information such as annual revenue. Having organized records and a clear picture of how your business operates will help insurers evaluate your risk profile accurately, which leads to more accurate quotes.

Platforms like Tailor Brands are designed to help business owners with this groundwork. From forming an LLC to keeping business information and documents organized, Tailor Brands offers a variety of essential services that small business owners need during setup and as they grow. With that said, it’s worth noting that coverage, pricing, and eligibility are determined by the insurer based on the specifics of your business, not the platform you use to form it.

Conclusion

General liability insurance is widely considered to be essential when starting a business because it addresses the types of claims that business owners are most likely to encounter: customer injuries, property damage, and certain legal disputes. While it doesn’t cover every possible risk, it provides a significant layer of protection against situations that could otherwise be costly.

Forming an LLC and purchasing general liability insurance serve different purposes, and many business owners benefit from having both. Understanding what general liability insurance does and doesn’t cover is the right starting point for making an informed decision about protecting what you’ve built.